The future for EdTech in India?

The future for EdTech in India?

Is EdTech going bust or is it going to make a massive comeback?

This is a part 1 of a 2 post series.

It’s been an interesting few months for EdTech as the headlines have changed.

Google search for “edtech in India” shows the following kind of results.

These are in addition to Amazon shutting EdTech in India, and various other such news.

Just one - two years ago; the flavor was very different:

So, what happened? Let’s dig in. Before we talk about why the fall let’s discuss the rise.

In early 2020, I predicted that India is going to see a huge flow of capital into EdTech. One part of the reasoning to believe this was:

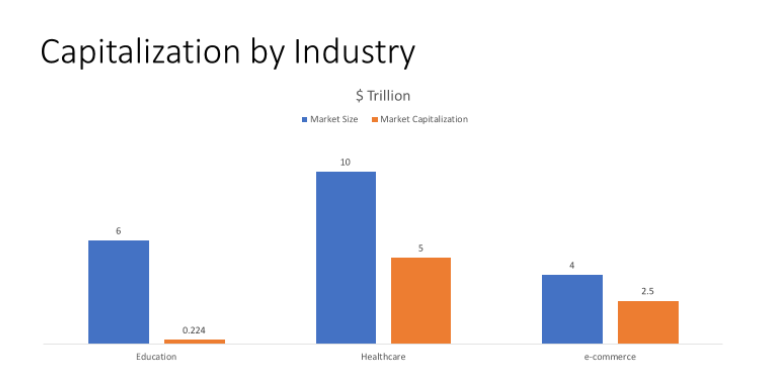

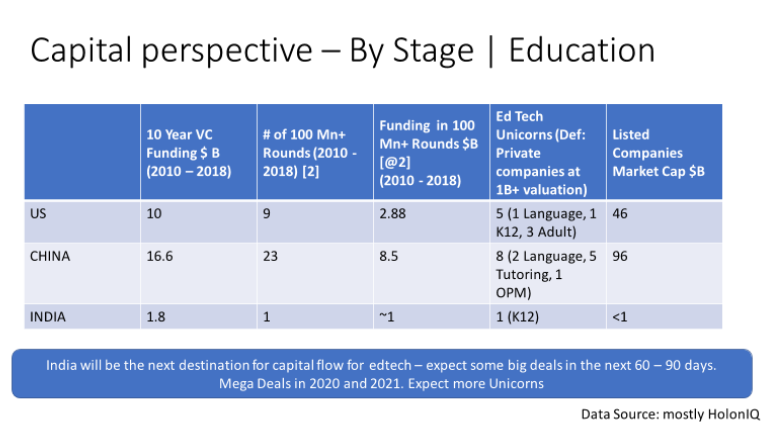

Indian EdTech Market was under-capitalized (still is)

Mega deals were coming because of under penetration in India, and the right timing

You can read the entire post and predictions here.

The second part of the reasoning was my visit to China in November 2019 and it became clear that China EdTech (largely K12) was saturated and overvalued; investors were looking at the next avenue and India seemed perfect, because of:

A large population

mixed market of K12 (including Test Prep) and Higher Education. Low potential for language learning unlike China. In some sense, bringing the best of China and the US (K12 and Higher Ed markets)

The Jio effect (for international readers: you can read how Reliance Jio’s cheap mobile data brought millions of Indians online)

And then:

There are decades where nothing happens; and there are weeks where decades happen"--Vladimir Ilyich Lenin

Covid hit us, causing a tizzy amongst offline players to move online.

and later, China cracked down massively on EdTech.

and they (the policies) include a ban on any for-profit tutoring services focused on the country’s core public school curriculum, oriented around the make-or-break high school and university entrance exams. Limits were also set on the times during which students could attend classes, restricting class schedules to no later than 9pm on weekdays, and allowing only extracurricular courses on weekends. - Techcrunch

So the capital flight started from China and the narrative started calling India the next EdTech opportunity.

Why China's crackdown on edtech companies augurs well for Indian startups - YourStory

Now, let’s see if my predictions held up?

In 2020, EdTech startups raised $2.2 Bn and it went up to $4.7 Bn in 2021

At last count, India had 7 EdTech unicorns

So what happened now?

Several pundits have proclaimed the death of EdTech in India, many naysayers have proclaimed that YouTube is better than most EdTech in India (and free), and VCs don’t want to touch anything EdTech anymore - especially if it is in K12, pre-revenue, or plans to change the world.

But let’s go beneath the surface and see what really happened while the frenzy was on.

Reasons for failure:

It was unfashionable to be profitable

Startups kept burning money and kept finding newer stories to support and raise more money. While this is dangerous in most startup's it’s even more dangerous in EdTech. Why? read on

GTM and CAC are real

I went to a startup conference a few months ago where a popular VC was telling the audience about how to calculate cash flow, estimate burn and runway and why it is important. I wish they had met the LIDO team before it crashed and burned.

Most startups - including many in EdTech - are unclear about GTM strategy and the devil of cost of acquisition (CAC). With increasing lead costs, easy VC money, and growth at all costs startups were hit badly once the party was over.

Contrary to popular perception, education is a local business and each segment and each geography are different than others. This is perhaps why India is home to regional players (Akash in North, and Chaitanya and Naraina in the South).

Here is a plug on my article on C.A.C which remains relevant to the day.

Outcomes

Parents have started focussing on outcomes as many players haven’t been able to prove the efficacy of their products. This is important in India where the focus on scores and ranks is very high. “For the love of learning” doesn’t cut it beyond a point. FOMO is real but then it doesn’t outlast true outcomes. It’s unfortunate that many EdTech startups haven’t taken the pain to measure or improve efficacy. A great opportunity lost. For test prep, while a subscription model is great but the purpose is not enjoyment like Netflix it is results and ranks.

Focus

Education is a specialized business and other than what Veranda is trying as a roll-up companies often are specialists in one to two areas. Imagine going to a specialist doctor vs a general physician; who would you consult in the case of a serious disease? Education like healthcare is the holy-grail, test prep is a highly intense and life changing event and so is which school you send your children to.

Queue for school admissions in India - Times of India

Hong Kong parents queue up as application period opens for preferred primary school spots - South China Morning Post

VC money

Damn you take it, damn you don’t. Too fast an expansion without an underlying growth story does create fuzz, a bubble and sometimes a lot more. But contrary to popular perception, VCs (and LPs) are in the business of being in a very risk asset class. So one man’s bold bet is another’s stupidity - no right answers.

Shift to offline

A lot of learners and parents are shifting their preferences to offline centers. Sometimes it is because of the physical proximity, other times because it brings a proctored learning environment for the learners, and in the case of adult learning the cool kids want to hang out with friends.

I have written about this in various posts before. A notable one to read is below.

So what’s the way forward?

Watch this space for the next post