EdTech Downturn

Is the party over in India?

Another day, another EdTech startup shuts down. It’s lately become the norm. If it’s not a shut down then it’s massive layoffs.

There seems to be, almost, no good news coming in.

Matrix backed crejo.fun has shut shop

SuperLearn stops operations as it’s not able to raise further

Byju’s, Toppr, WhiteHat Jr have fired more than 2500 people

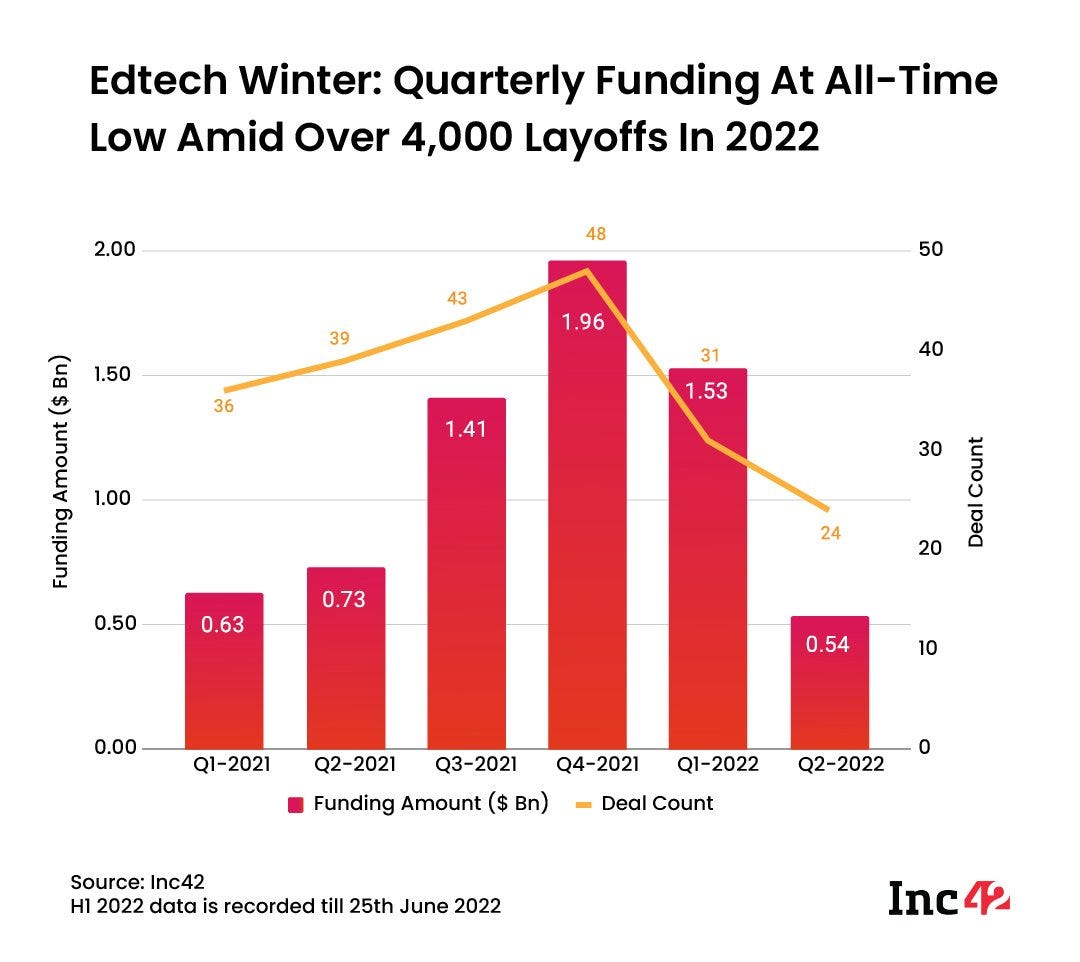

Inc42 calls it an EdTech winter and says that “On a quarterly basis, the funding in edtech has plummeted from $1.4 Bn in Q1 to $537 Mn in Q2 2022, a massive drop of 61% for edtech funding”

And then there are a few exceptions:

UpGrad has raised a round at a valuation of $2.2 Bn

PhysicsWallah or PW became India’s 101st Unicorn by raising $100Mn Series A

Edtech Startup Leap raises $75M in Series D round led by Owl Ventures

EdTech Startup EdSARRTHI, a Mentorship Platform Raises Seed Funds

There is also an opportunity, perhaps?

Abhimanyu Saxena of Scaler told Economic Times that their $55 Million Series B fund-raise from Lightrock India is “to create (a) war chest for the inorganic growth opportunities we see in newer markets such as the US”. He further said that “In 2022, we will focus on India as well as the US market and then will look at other markets, such as Latin America and SouthEast Asia”.

Edtech startup BrightChamps is planning to close mergers and acquisitions worth $100 million through stock and cash deals in the ongoing fiscal year (FY23), co-founder and chief executive Ravi Bhushan told ET. He further added, “The acquisitions will likely be across India, the United States, the UK, the Middle East, and Southeast Asia.”

And, Byju’s is looking to acquire 2U for a whooping $1Bn at a share price of $15 which is a significant premium to its share price of $9.3 reports Inc42. The share price, BTW, has already climbed up to $12.25 since the announcement but it’s nowhere close to the 5-year high of $98.08 or 52-week high of $46.52. Notable to say that there are questions about Byju’s ability to fund this deal given that The Morning Context, and Quartz have reported that Byju’s has faltered on/delayed payment commitments for its acquisition of Akash.

Are these good deals? Will the Indian companies with global ambitions be able to acquire and integrate these companies well? These are both separate posts in themselves and perhaps I will get into them soon. But, thoughts on this welcome on this post or on Twitter. The key question, for now, is why this sudden rush to acquire companies? Is it the time to raise capital if you are successful and have access and look for distressed assets, or is it the best time to go global as the world becomes flatter, or is the India EdTech story itself saturated? Let’s try to assess this.

First, it’s important to add more color to what’s happening in Indian EdTech.

Is the downturn in EdTech permanent?

Here is an interesting view from Akhil Kishore.

I have been at the end of seeing two such cycles in India. The first one was the Educomp effect; where suddenly - thanks to its public numbers of extremely high EBITDA and ~74X return delivered to one of its late-stage VCs - there were 40+ competitors in the space. Only a handful of those competitors exist now and are either distressed or are very small. Yet, it put considerable pressure on Educomp and we know what happened. I know, I know what you are saying right now. The diversification into many businesses, trying to create an education ecosystem, securitizing revenue, picking up huge loans, shortage of cash, and ultimately bust with allegations of fraud.

Except for the last two aren’t the same things being said about Byju’s recently? Tough not to draw parallels here. But the point is that Byju’s has made some smart moves - by acquiring Toppr (for outcomes), Aakash (for its flywheel, cash flow), and Great learning (for diversification) and now hopes to fuel its global ambitions with 2U’s possible acquisition. There is an interesting narrative that the Ken has put out on this - and the possible Chegg acquisition - but we will get to it in a separate post as I said earlier.

The key points here are:

Nothing is permanent whether it’s up or down | every industry goes through cycles. The cycles (and hypes) are deeper when venture capitalists get involved. So it’s naturally some of the froth going away

There is a shift - especially for K12 - with consumer preferences changing back to offline as the world opens up and we learn to live with the virus. So, it’s a shift of revenue from EdTech back to Education

Read more about the shift in my two-post series given below. Particularly, interesting is the point that what was the expected longevity of these shifts? Did the VC’s price this in the valuations or not? Did K12 become overhyped with too many startups in the space - selling coding, maths, English, music, and what not?

Finally, back to Akhil Kishore and what he advises for the future.

Market impact on EdTech is it across all sub-sectors?

It’s interesting that each time markets swing in a direction they go all the way. From the funding frenzy to the funding winter.

Is EdTech really dead or is hybrid the new norm? Are there sub-sectors that are isolated and should be something that one should look… all topics of future discussion.

Source: Kaltoons.com